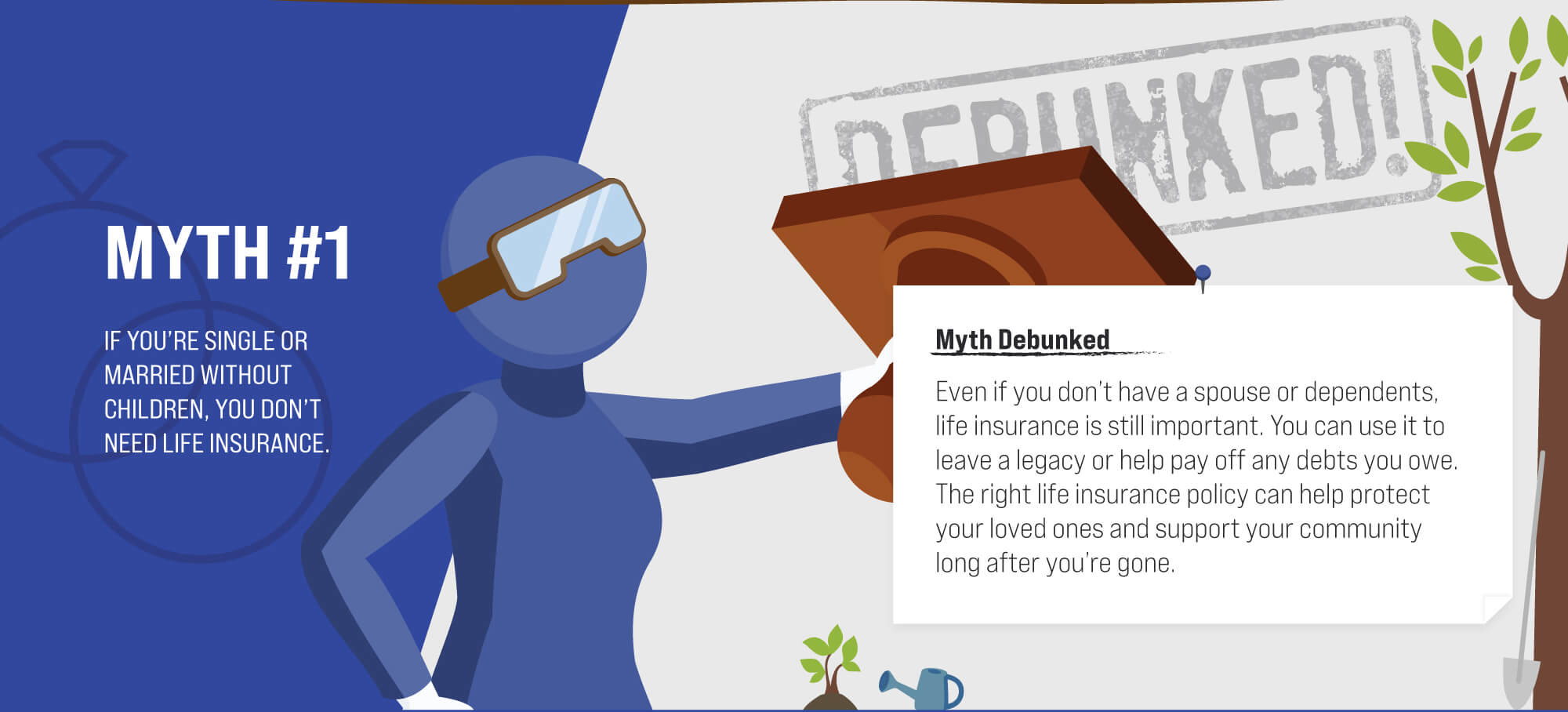

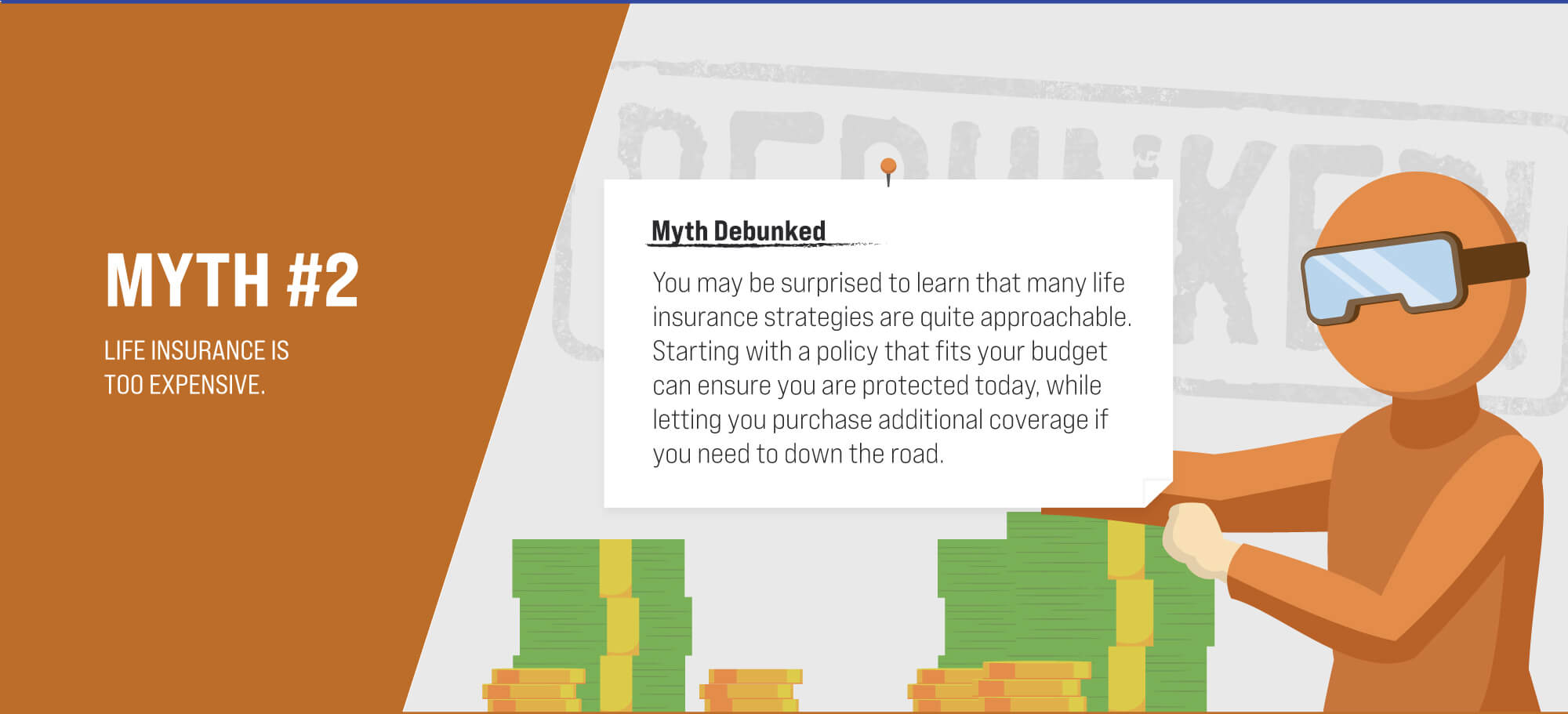

Life Insurance Myths: Debunked

Drinking may be a “rite of passage” for teens, but when it occurs in your home you may be held responsible for their actions.

If you want to avoid potential surprises at tax time, it may make sense to know where you stand when it comes to the AMT.

Understand how SECURE Act 2.0 affects RMDs and how using a QCD can possibly benefit both taxes and charitable goals.